Market Report: Technical rally holds

Nov 4, 2016·Alasdair Macleod It has been a better week for gold and silver, with gold rising from $1284 to $1302 by Friday mid-morning London time, and silver from $17.76 to $18.34.

It has been a better week for gold and silver, with gold rising from $1284 to $1302 by Friday mid-morning London time, and silver from $17.76 to $18.34.

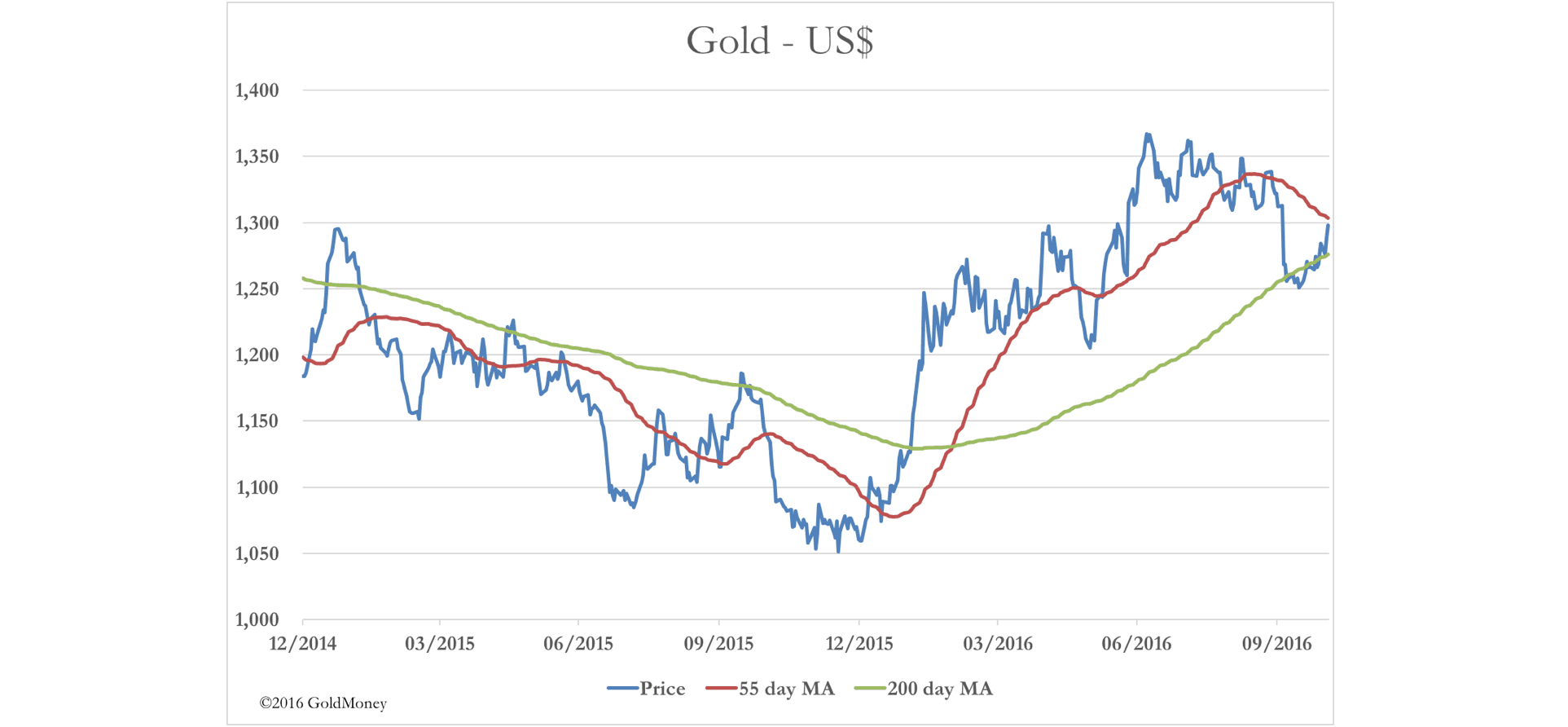

Gold in particularly found its support at the 200-day moving average, and has run into some predictable profit-taking at $1300, which is also the approximate location of the 55-day moving average. This is shown on the next chart.

Technically, some consolidation at this point makes sense, so that an assault on overhead supply between $1315-$1350, evident on the chart, might have a good chance of success.

In the absence of other considerations, this chart should be a reasonable guide to likely prices on a one to three-month view. However, there is much bubbling just under the surface. The US Presidential election is taking an unexpected turn, with the Clinton camp being torpedoed by the FBI, which has renewed its investigations into the email scandal. The S&P 500 index has broken the important 2120 level, and is now struggling to hold 2000. Bond yields have dropped slightly this week, with the US 10-year Treasury now yielding 1.812%, after having risen 50 basis points since July.

Traders are interpreting these moves as a response to increasing uncertainty over the Presidential Election. It certainly makes sense on a safe-haven trade to sell equities, buy bonds and gold. But sense is subjective, and explanation of price moves are usually little more than an attempt to match price moves with news headlines.

This risk-on trade tied to the election news might make sense, but it ignores the build-up of armed forces between NATO and Russia in Eastern Europe, which is a lot more important in the scheme of things, than the Presidential election. One can easily visualise central banks and regional sovereign wealth funds acquiring physical gold as protection against geopolitical tensions.

Dollar interest rates

The talk of an increase in the Fed Funds Rate in December remains, and there have been hints from FOMC hawks that it is now more than likely.

This prospective event has been more widely advertised than a new hit musical on Broadway, as was the rise of 0.25% in the target rate last December. That event marked the end of gold’s bear market, and it could be that once the December rise is out of the way, gold will rally again, for the same reason, i.e. it has been over-discounted.

Anyway, precious metals became somewhat oversold in October, so the absence of bad (or should it be good?) news has been enough to sustain a decent technical rally. The key as to whether or not it will have legs for a further rise is perhaps found in the actions of long-term investors, whose exposure to gold is generally very low. Many of these actors have been looking for a pull-back so they can buy, and they have now had it. However, the speed of the rise will have caught most of them by surprise, suggesting that they might be forced into buying on rising prices from here.

Driving this potential interest in gold includes the lack of alternatives. With equities highly priced and bonds susceptible to the Fed’s likely interest rate rise, investors are very sensitive to politics, and the uncertainty of a close result in America. And if the politics are uncertain, can the Yellen put still be relied upon?

The views and opinions expressed in this article are those of the author(s) and do not reflect those of Goldmoney, unless expressly stated. The article is for general information purposes only and does not constitute either Goldmoney or the author(s) providing you with legal, financial, tax, investment, or accounting advice. You should not act or rely on any information contained in the article without first seeking independent professional advice. Care has been taken to ensure that the information in the article is reliable; however, Goldmoney does not represent that it is accurate, complete, up-to-date and/or to be taken as an indication of future results and it should not be relied upon as such. Goldmoney will not be held responsible for any claim, loss, damage, or inconvenience caused as a result of any information or opinion contained in this article and any action taken as a result of the opinions and information contained in this article is at your own risk.