Market Report: Mirror reflection of the dollar

Aug 12, 2016·Alasdair Macleod

Last Friday (5 August) the US dollar jumped on better than expected payroll figures, and spent the first half of this week easing as the excitement wore off, before rallying again yesterday.

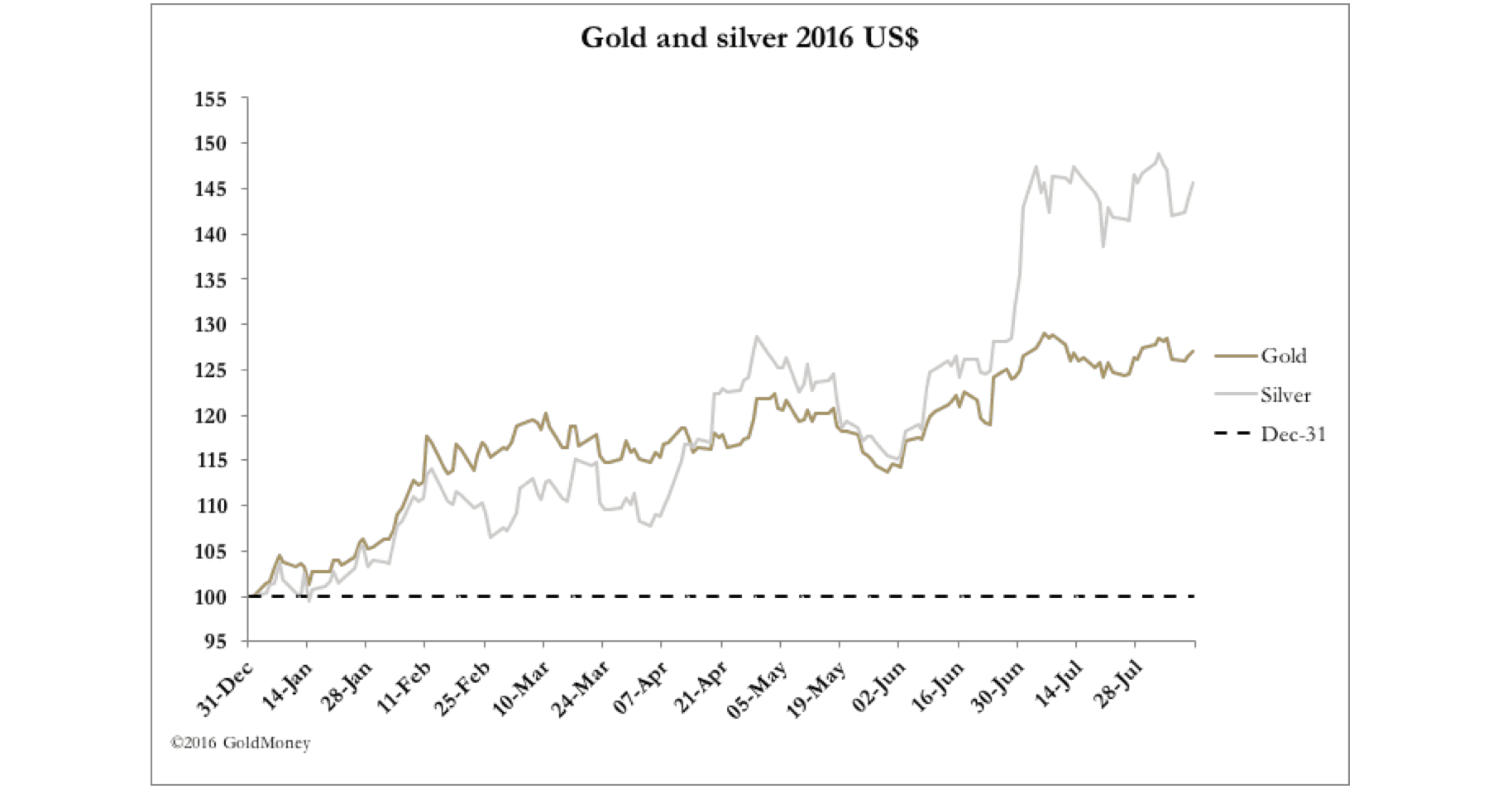

Gold and silver reflected these moves in reverse, falling heavily last Friday, recovering two-thirds of the fall by Wednesday’s US opening, then falling back yesterday. Gold rose only $7 net from Monday’s opening of $1333 to $1340 by early this morning UK time (12 August) and silver by 40 cents from $19.60 to $20.00.

Gold has essentially paused, the moves being a mirror-reflection of the moves that are coming from the dollar side of the price.

Of the major currencies gold measured in sterling has risen most this year, and sterling’s continuing weakness against the other currencies continues this relative trend. This is clearly seen in our next chart.

The downturn in the yen price of gold reflects the yen’s continuing strength, with the rate having fallen from 120.6 to the US dollar to under 102 since January 1st. There is little sign of this trend ending, and of the psychological 100-yen level looks likely to be breached in time.

This is partly because Japanese insurance and pension funds now find that investing in US Treasuries does not produce a positive return after currency hedges, so there is little point in them doing so. Outward investment flows are therefore diminishing. The upshot is that for Japanese investors, gold is getting cheaper relative to alternatives, which should encourage investment in physical jewellery where price matters, and to a lesser extent perhaps, physical bullion where the trend matters more.

The gold futures market is still overbought, but less than it was, reflected in the fall in Comex open interest from 11th July. This is shown in our next chart.

By historic standards, OI is still high, reflecting the large swap and bullion bank shorts. This is certainly the case in the forwards market in London as well, where the bullion banks run a fractional reserve system based on a small amount of gold backing extensive customer liabilities. The only protection for them against sharply higher prices is to buy out-of-the-money calls on the over-the-counter markets, with strike prices somewhere over $1400. In effect, these call represent a reinsurance policy against financially life-threatening losses.

The bullion banks have abandoned their forecasts earlier this year of sub-$1,000 gold prices, not least because of the continuing spread of negative interest rates and bond yields. That being the case, they will wish to use summer trading lulls to work prices lower in the hope of either closing their short positions, or buying cheaper OTC calls.

That is what working Comex open interest lower is all about. For traders it is a game of patience, knowing that time expiry works against the speculators. That being said, the world’s financial problems are intensifying, and ratcheting up the stakes.

Our last chart is of the gold price in USD, with the moving averages that technical analysts use to gauge medium to long-term trends.

Both moving averages are moving strongly upwards in bullish formation, and the closing gap between the 55-day MA and the price limits the downside to the $1300 level, and it looks like even that is unlikely. Whatever the short-term outlook, it appears that the gold price is girding its loins for an attack on $1400, on its way towards $1500.

The views and opinions expressed in the article are those of the author and do not necessarily reflect those of Goldmoney, unless expressly stated. Please note that neither Goldmoney nor any of its representatives provide financial, legal, tax, investment or other advice. Such advice should be sought from an independent regulated person or body who is suitably qualified to do so. Any information provided in this article is provided solely as general market commentary and does not constitute advice. Goldmoney will not accept liability for any loss or damage, which may arise directly or indirectly from your use of or reliance on such information.