Indian gold jewelry demand reacts to prices, not vice versa

Nov 10, 2016·Stefan WielerIndian gold jewelry demand reacts to prices, not vice versa

Introduction

For the past weeks the media and gold analysts have pointed to an apparent collapse in Indian gold demand, implying that gold prices are at risk. However, Indian gold demand doesn’t drive prices; rather, prices drive Indian gold demand. When gold portfolio demand in the financial markets increases (as real-interest rates and currency values decline), traditional buyers in the developing markets that buy gold as a form of savings correspondingly have to reduce quantity demanded (but not value demanded). However, India’s decision yesterday to recall all 500 and 1,000 rupee banknotes overnight might mean Indian savers might not be willing to give up their gold savings all that easily, demanding a higher proportion of their own portfolio allocation from yet another relative currency risk.

View the entire Research Piece as a PDF here...

A barrage of media and research reports highlighted the apparent collapse in gold demand from the Indian jewelry sector over the past few weeks.

Bloomberg reported on October 24, 2016, that Indian gold demand was set to drop a staggering 25% this year to just 650 tonnes from 864 tonnes in 2015. Poor monsoon rain, the Indian government’s crackdown on tax evasion and a strike by jewelers protesting a newly introduced excise tax on jewelry made and sold in the country are cited as reasons and several sources state the dire state of the market.

All this implies that gold prices are at risk of sharp declines here as demand from the largest importer is seemingly collapsing. However, this argument completely confuses causality.

Understanding to role gold plays in a portfolio is key, be it a “western” financial portfolio or that of hundreds of millions of distributed Indian households. Gold is simply a money stock in these portfolios—not a luxury good or commodity—an inventory that stores value and effortlessly maintains commodity-purchasing power against exogenous inflationary pressures. Gold should always be analyzed from this perspective, be it in the form of “savings jewelry”, coin, bullion, or pooled EFT, as this is how it is understood by the vast majority of humans demanding it. All else equal, for quantity demanded in India to hold flat year over year against a 20-25% increase in the value of gold (or decrease in the relative value of currency), Indian income in Rupee terms would have had to increase 20-25% year over year as well, as Indians simply accumulate gold jewelry (or savings/inventory/money stock) with income over time.

The problem is that most analysts still look at the gold market the same way as they look at commodity markets generally, where prices are driven primarily by changes in inventories. Simply speaking, rising inventories are negative for prices and vice versa (It is a bit more complex than that and for those who like to fully understand the relationship between prices and inventories we recommend reading our framework note Gold Price Framework Vol. 1: Price Model, October 8, 2015). The author of this report has worked as an oil analyst for most of his career. In order to predict whether inventories are set to rise or fall, oil analysts would try to forecast future oil supply and demand. Future supply predictions take into account how depletion rates will evolve and what new oil projects are coming online. Future oil demand is mostly a function of economic growth in the short term and technological shifts in the long run. The residual in the model then are the inventories - if forecasted supply exceeds demand, inventories are expected to increase. The key takeaway from this is that in the commodity world, physical demand matters. It is what changes inventories and thus drives prices. If data shows that Chinese oil demand is falling off a cliff, oil analyst rightfully should get bearish as then this implies rising inventories and falling prices. Eventually the change in price will impact supply and demand and bring it back to balance at a lower price.

However, analyzing gold in this way is invalid. Gold, unlike a commodity, is never consumed. Once it has been mined, it is always stored in some way. Hence, when we speak about “demand” for gold, this has nothing in common with demand for a commodity. In the commodity world, demand means consumption. For example, crude oil is bought by refineries, turned into gasoline, sold to consumers and burned in a combustion engine. The oil is irrevocably consumed. In comparison, most of what is referred to as gold “demand” is from jewelry, bullion, coins and bars, which are just different forms of inventory. Even the small amount of gold “demand” from the industrial sector and from dentistry is not equivalent to consumption as almost all of that gold is later recycled.

The same rationale also applies to supply. When we speak of supply of a commodity, it always means production from a mine, a well or an acre of arable land. While gold supply also comes in the form of new mine supply, most gold flows throughout the year simply reflect existing gold in inventory that changes ownership. In the commodity world we would never call this supply. Oil that has been stored in a tank in Cushing Oklahoma is simply inventory. No oil analyst would ever come up with the idea to treat a sale of this inventory as supply. Yet in the gold world, analysts do that all the time. About one quarter of the annual “supply” in the standard gold balance sheets is coming from recycled gold, often referred to as scrap gold. It’s mostly jewelry and medallions that are sold, melted down and turned into new jewelry, bars and coins. It was inventory before and has become inventory again. With the same rationale, the millions of tonnes of gold bullion that are traded each year would have to be treated as supply as well. The only difference is that those bars are not re-casted.

Hence to model the gold market in terms of “flows” equivalent to a commodity market is invalid and leads to erroneous conclusions. This doesn’t mean that collecting an analyzing this data is meaningless, quite the opposite. For example, understanding trends in mine supply is key for the gold market. But trying to apply a commodity price model to a gold balance table simply won’t work.

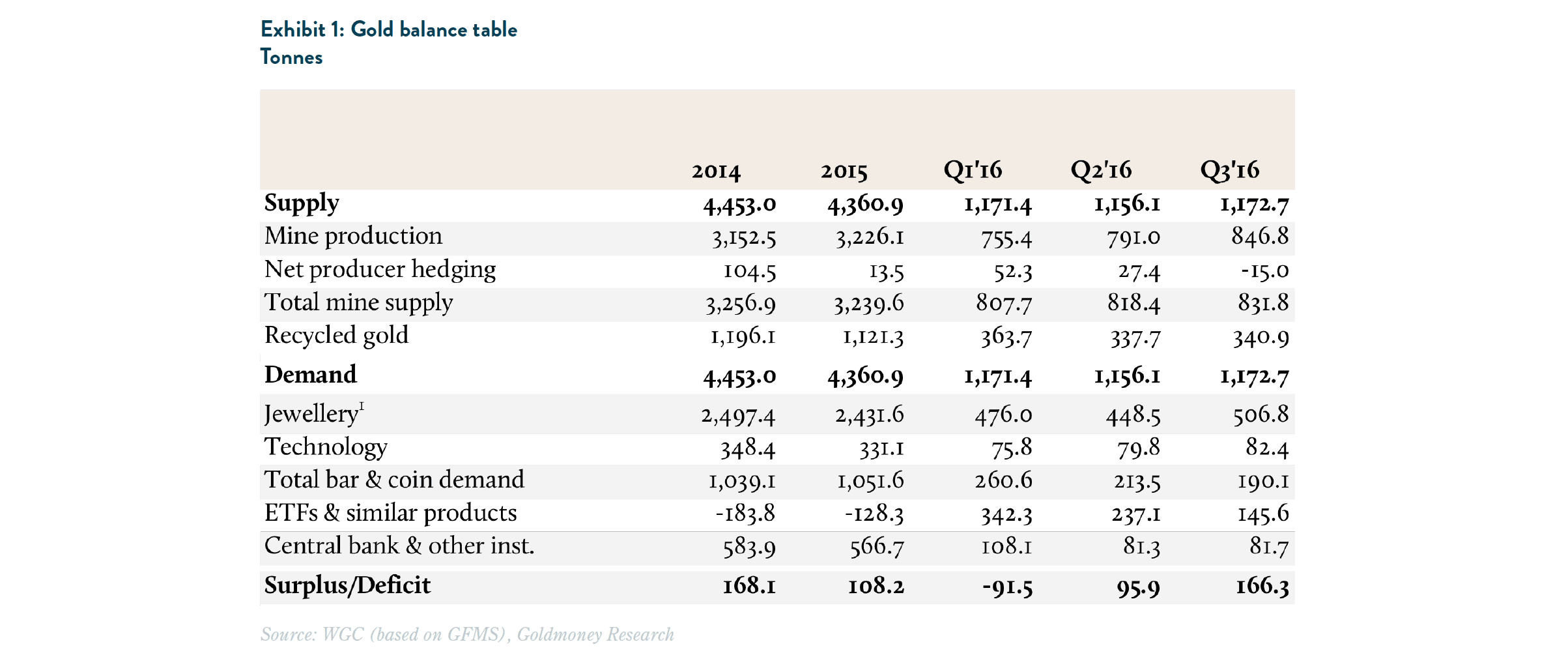

In order to fully understand why modeling gold “flows” does not help understanding price changes, we need to look at a typical gold balance table (see Exhibit 1). Typically a gold market balance shows supply in the form of mine supply and recycled gold. On the demand side, it would show jewelry, coins & bars, central bank net purchases, industrial demand (including dentistry), ETFs and a residual. The World Gold Council reports a gold balance based on data from GFMS, a global economics consultant for precious and industrial metals. In the GFMS balance, the term used for the residual changed several times over the years, from “balance” to “inferred investment”, “OTC investment and stock flows” and currently “surplus/deficit”. This demonstrates the dilemma of trying to model gold like a commodity. The residual reflects how much inventories of bullions at exchanges and over the counter have changed. In a commodity balance, that would be the one number every analyst would try to predict, because that is what drives the price. But in the gold market, everything is inventory1. Hence the residual shows just changes in one of many inventory categories. That is why GFMS could not simply call it inventory, like in every commodity balance.

A gold balance basically just shows how much gold was mined in a given time period and how much gold was turned into jewelry, bars, coins, dental implants and electronics. But within those categories, there are massive flows. In the London Bullion Market (LBMA), more than USD240 billion of gold is traded every day. That is equivalent to close to 2 million tonnes a year. Correctly, gold balances based on flows would have to show all of these movements as well as supply and demand2, but none of them does.

It is key to understand that some sources of “demand” in the gold balance are price markers and some are price takers. When we think of gold jewelry we typically think of expensive watches and designer-necklaces. However, most jewelry is produced with a small markup over the gold price and bought as savings in emerging markets such as India. It’s very different from gold jewelry in the west where the manufacturing and branding costs often exceed the value of the gold. A large part of the Indian public has no other way to save money than in gold. They often lack access to bank accounts and inflation leads to a constant decay in purchasing power. Thus Indian farmers and other laborers will simply turn their profits or wages into gold. Most of it will be in the form of jewelry, but it also comes in the form of coins (medallions) and small bars. To our knowledge there is no standard name for this source of demand in the gold industry. For simplicity we call this “perpetual savings demand” for the remainder of this report. It’s a permanent source of gold demand. Importantly, when the INR depreciates, wages and profits of farmers don’t catch up right away. Hence as gold prices go up in INR, Indian gold jewelry buyers can simply buy less gold (yet the same amount in INR). 2016 is a prime example. Indian jewelry and coin demand might be down 25% but gold prices are up 20% year-over-year.

Thus most jewelry buyers are price takers not price makers. There is no sudden spike in jewelry demand that pushes prices higher. Developed world gold demand tends to be different. Most western households don’t permanently turn their currency into gold for savings purposes, at least not yet. In the developed countries, gold demand tends to increase with falling real interest rate expectations as gold competes with currencies. But in the Western hemisphere this demand doesn’t come primarily in the form of jewelry but in what is typically – and falsely - labeled as “investment demand”3. It includes ETF holdings as well as the residual which is OTC bars and coins and changes in Exchange inventory.

Mine supply is very stable over the short and medium term. Therefore, when “investment demand” rises, somebody else has to give up some of their gold (demand) in return4. Industrial demand including dentistry is very price inelastic and changes in central bank gold holdings are driven by political decisions and not price. Hence almost by definition, when “investment demand” goes up, “perpetual savings demand” (hence jewelry) correspondingly has to go down.

Below we have plotted changes in “perpetual savings demand” vs “investment demand.” Note that the GFMS balance does not differentiate between developed market bar and coin demand and developing market bar and coin demand. The former would be considered “investment demand”, the later “perpetual savings demand”. Hence we plotted two charts: Exhibit 2 shows Net jewelry demand (net of recycled gold plus coins & bars) vs the inverted (ETFs and the residual). Exhibit 3 shows the same thing but coins & bar demand was included in the “investment” category rather than the “perpetual savings” category. Both charts show that “perpetual savings demand), (hence jewelry) goes down when “investment demand” goes up.

Importantly, the mechanism by which jewelry buyers reduce their gold purchases is simply the price. When real-interest rates fall, “investment demand” - mainly from the developed markets - increases. Prices need to go up to convince jewelry buyers in the developing economies to give up some of their demand. This works on a global basis measured in USD (see Exhibit 4) and specifically for Indian demand, measured in INR (see Exhibit 5).

We thus conclude that changes in Indian jewelry demand are not a good predictor for prices. Rather, Indian jewelry demand changes because prices have changed. This year gold in INR is up 20%, mainly because gold prices are up 20% in USD rather than due to a devaluation of the INR.

The increase in gold price in USD came on the back of a sharp increase in “investment” demand where ETF holdings are up 640 tonnes since the end of last year.

Does this mean that Indian gold demand does not matter at all? No, when Indian gold demand changes for reasons other than price, it can certainly matter. The previously mentioned excise tax introduced earlier this year certainly has the potential to take out a chunk of demand that exceeds what is incrementally bought in the developed markets as it simply increases the price beyond where the two would perfectly offset. However, as the excise tax is potentially a negative, the latest developments in India point to an entirely different direction. BBC reported yesterday that India has suddenly decided to call in all 500 and 100 rupee bank notes overnight. Apparently banks were closed on Wednesday and ATM machines were not working. New 500 and 2000 rupee denominations will replace the old notes which can be exchanged within the next 50 days, but all exchanges will be monitored closely. What can be seen as another strike in the global war on cash is officially a measure to counter “black money” and corruption. Due to many Indians’ deep suspicion of government motives around monetary and banking policy generally, it also has the potential to lead to a sudden surge in Indian gold demand that could more than offset any weakness due to the tax. Our sources report that the surprise move has turned the Indian retail market into a frenzy. As seen elsewhere in gold’s most important price drivers: energy prices and real interest rate expectations, the asymmetry in Indian gold demand has now shifted to the upside.

View the entire Research Piece as a PDF here...

1.With the exception of mine supply

2.Which would be overwhelmingly large compared to the amount of gold that is transformed into jewelry each year.

3.The notion that gold is an investment is wrong. Gold is money and people want to hold more or less gold relative to currencies when real-interest rates of these currencies change. For the remainder of this note we continue to use the term “investment demand” to describe this source of demand

4.The difference to commodity markets is that supply and demand don’t have to be in balance all the time as inventories can build and draw. But the gold balance is basically pure inventory data. So if one inventory goes up, another has to go down if the increase exceeds new mine supply.

The views and opinions expressed in this article are those of the author(s) and do not reflect those of Goldmoney, unless expressly stated. The article is for general information purposes only and does not constitute either Goldmoney or the author(s) providing you with legal, financial, tax, investment, or accounting advice. You should not act or rely on any information contained in the article without first seeking independent professional advice. Care has been taken to ensure that the information in the article is reliable; however, Goldmoney does not represent that it is accurate, complete, up-to-date and/or to be taken as an indication of future results and it should not be relied upon as such. Goldmoney will not be held responsible for any claim, loss, damage, or inconvenience caused as a result of any information or opinion contained in this article and any action taken as a result of the opinions and information contained in this article is at your own risk.