Gold – a primer for 2017

Jan 19, 2017·Alasdair MacleodYou know when to buy gold: it’s when nearly every trader and commentator tells you that gold is going lower and you should sell it.

This is Harry Dent on 10th January: “I still see gold landing somewhere between $650 and $750 in the next year or so” i. Dent invokes Elliott Wave Theory. EWT states that a bull market is comprised of impulse waves of three separated by two corrective ones, totalling five all together. Bear markets are made up of three waves, two impulse in the direction of the bear trend, separated by one consolidating countertrend.

I am simplifying the theory considerably to make a point, but I do know my onions, having in the past taught, examined and lectured on EWT on behalf of the UK’s Society of Technical Analysts. Ralph Elliott only applied his theory to equity markets. Reflecting the greater value over time placed on stakes in human progress, it makes sense. It is modern chartists who have extended its use to other markets.

But money and currencies? The first decision you must make is which of the two variables in a price is in a bull market. It is commonly thought gold is the variable, but the chart below illustrates the problem is more likely fiat currencies priced in gold.

The four currencies shown, including the dollar, have been firmly in bear markets since the year before Bretton Woods was abandoned. Note also that the price scale in the chart is logarithmic, so these are enormous losses for fiat currencies. So, Dent and his fellow-travellers are effectively using a theory that was never intended to be used outside equity markets to recommend their clients and subscribers play a counter-trend rally that’s already over five years old.

Elliott theorists are also oblivious to a mathematical impossibility. If a currency is deemed to be in a bull market, it moves up in fives. If the other currency being measured against it, or commodity if you must, is in a bear market, it moves down in threes. How can one be moving in fives, while the other moves in threes? It cannot, it is a story of square pegs and round holes, and wholly disqualifies EWT applied to gold.

You cannot rule out the possibility that gold will go to Mr Dent’s $650 to $750, but for that to transpire I suggest two things would have to happen. Interest rates would have to be raised beyond the point where bad debts and falling bond prices break the banks, and the Fed would have to convincingly signal to markets that it is prepared to stand aside and let the banks fail. I believe these two conditions to be extremely unlikely. In the event of an interest-rate induced crisis, it is far more likely the Fed will repeat the successful formula (from the Fed’s point of view) of providing unlimited credit, as it did post-Lehman. A pathological fear of deflation ensures the outcome. And unlike the time of the Lehman crisis, investors will know the solution in advance, and their response will differ accordingly.

It was the post-election move in gold that wrong-footed everyone. A Trump victory was quickly turned from an event that brought with it heightened uncertainty, to one that promised higher interest rates, higher bond yields, and a strong dollar. The winners in this about-face, in the gold contract on Comex at least, were the bullion banks, which were very short. It suited them to drive gold and silver lower to close their short positions, and/or show favourable year-end book values. Amateurs in the game, who are nearly always caught out by the bullion banks’ periodic bear-raids, take the aggressive fall in prices as evidence that they should panic at what often ends up being the bottom of the market.

These banks are still short, having not managed to buy back all their positions, which is probably one reason why the current rally is so strong. And things are not looking good for the bullion banks, with prices running away from them with only a partial increase in open interest. As can be seen in the graph above, measured in gold the dollar has lost 97% of its value since 1969. If the dollar was a stock, informed opinion would be that it is bust and should not be bought. The same would be true of sterling, which has lost 98.5%, and the euro (including its components before 2001), down 98%. The legendary trader of yore, WD Gann, reckoned that any stock that fell to less than ten per cent of its high was probably bust, and should be avoided. It’s a good rule of thumb, and on that measure, not even the yen has a future.

The confusion for investors seeking guidance from so-called experts is they are always presented with charts showing gold priced in dollars. The immediate and unwritten assumption is that it’s the gold price that moves, and the currency is constant, overlooking the fact that the dollar persistently loses its purchasing power, confirmed by the almost continuous increase in the consumer price index. Showing gold priced in dollars, or any other currency for that matter, also encourages the myth that gold is an investment which either outperforms or underperforms cash. Technically, gold is not an investment. It is either a commodity, money or both, depending on your point of view and how you define things. Almost all financial commentators, including most gold bugs, make this very basic mistake.

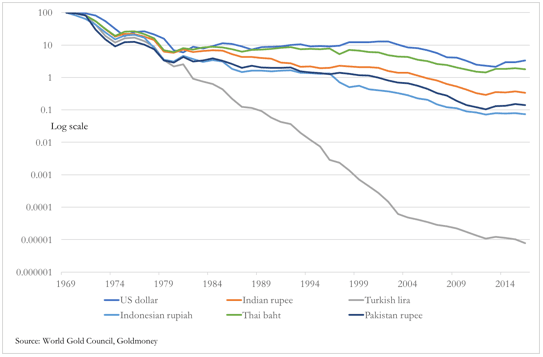

Another myth that must be addressed is that gold is no longer money. For most of the world’s population, it most certainly is money, mainly because of its superior qualities as a store of value. Our second chart shows what has happened to selected Asian currencies over the same time-frame as the first chart, and includes the US dollar for comparison.

A Turkish national, holding on to his lira, has lost 99.99999% of his purchasing power measured in gold. An Indonesian has done somewhat better having lost 99.92565% on his rupiahs, but we are splitting hairs. The point is, does anyone seriously think the nearly two billion people behind this sample regard their governments’ fiat currencies as having any use beyond a means of rapid exchange?

Obviously not. Gold will always be regarded by all Asians as the preferred money, to be bought and held by selling the fiat. The only people who argue that gold is no longer money are Western-educated economists and their followers, having influence over an audience which mostly doesn’t care one way or another. These economists and their epigones probably number no more than a million or so, being a percentage of the global population that is not too remote from the percentage losses an Asian has suffered by holding on to his national currency.

The economists’ motivation is not so much a search for the truth, but more of a consequence of the sponsorship of their education by governments, and subsequent employment by both government agencies and a compliant financial establishment. Economists are like the three wise monkeys in their support for government currencies. The United States government does not want to see any challenge to its primacy over issuing the world’s reserve currency, and does everything to protect it, with a special dislike (or is it fear?) reserved for gold. Therefore, establishment economists dance to this tune, and are paid to do so.

The US Constitution explicitly states that gold and silver are money, yet since President Roosevelt banned the ownership of gold coin, gold bullion and gold certificates in 1933, US citizens have been denied this constitutional right. Few complain. Furthermore, when US citizens were once more permitted to own gold, any notional profits arising from the dollar’s debasement has been deemed profit and subject to tax on capital gainsii.

It is no coincidence that the dramatic declines in purchasing power for all fiat currencies, in addition to those illustrated in the two charts included in this article, stemmed from the time the dollar’s purchasing power could no longer be maintained at $35 to the ounce. The collapse in fiat currencies’ purchasing power since then has been in two broad moves, the first in the 1970s and the second from 2002 to 2011. Yet still, we have the establishment mainstream in financial markets claiming that gold is not money, and every time the dollar pathetically rallies from its deathbed against gold, they chorus “We told you so”.

Eurozone demand could be the surprise for 2017. The influence of Western-centric ignorance will probably be tested again later this year, as the Eurozone desperately tries to preserve its future and that of the euro. Only this week, President-elect Trump fired a starting gun on the EU’s political disintegration, by offering Britain and any other leavers quick and practical trade deals. This is a major about-turn from American post-war policy towards Europe. The change of policy is all fine and dandy, but it could be a trigger for the end-game of a financial mess in the Eurozone, whose resolution looks insoluble without massive monetary expansion. No wonder prescient Germans are already accumulating gold, and there can be little doubt that other EU nationals will increase their hedging against the euro’s ultimate failure as well, because that failure is becoming more likely by the day.

Sophisticated ignorance over gold goes one step deeper as well. Many commentators, knowingly or unknowingly, form a judgement based on their interpretation of the charts, and then select from a range of fundamental arguments to suit. Take India, where the currency has been mostly withdrawn. Recorded gold demand will presumably fall because there is little currency available to the unbanked masses for payment. This ignores unrecorded increases in smuggling, stimulated by the enhanced risk to the purchasing power of the rupee, already down 99.67% since 1969. Add to this stories that China has been restricting import licences for gold. For the chartist, the two largest sources of demand for physical gold are conveniently removed from the market. Throw in a strong dollar, and how could anyone argue against a falling gold price?

Except, since Harry Dent made his prediction on January 10th, gold has risen inexorably, despite these negatives. At the very least, he and his ursine tribe are being badly squeezed. What should worry these people even more is that the dollar’s falling purchasing power today against gold is driven by physical demand for bullion, and is despite the dollar’s strength against other fiat currencies.

Some important physical buyers appear to be waking up to the inflation and currency risks ahead. It should be clear to any intelligent observer that 1.3 billion Indians will chase up food prices later this year, because crops are not being planted through lack of cash. Monetary inflation in China is likely to lead to rising prices for a further 1.4 billion Chinese. Property bubbles abound throughout Asia, with new skyscrapers going up everywhere. It is redolent of the conditions that led to the Asian crisis in the late nineties, on a grander scale.

Crucially, measured in dollars the strength of energy and raw material prices throughout 2016 was an early warning of future price inflation everywhere, and expanding bank credit in America is fuelling the trend as well. The conditions for a reversal of the forty-year trend of declining price inflation are now in place, negating any bearish argument against gold. We don’t know who is actually buying physical gold, suffice to say the really big money has very little exposure. But now that the status quo is being challenged and price inflation is back on the agenda, central banks and other big buyers now find gold attractive.

I have written at length elsewhere about how price inflation is going to be a growing problem, and how restricted the Fed is in responding to it. The danger is increasingly being recognised by the other commentators. Additionally, Trump’s planned economic stimulus is unfortunately timed, coming on top of an economy that is being successfully inflated by expanding bank credit. Instead of declining, gold has every reason to go considerably higher, measured in those continually depreciating fiat currencies.

i See http://economyandmarkets.com/markets/gold/harry-dent-gold-recent-bounce-temporary-trend-still-down/. Dent is on record predicting a gold price of $250 in 2014. He appears to base his predictions on a combination of reading cycles and Elliott wave theory.

iiUS residents may be interested in the “Make money great again” campaign to recognise gold and silver freely used as money. See https://www.mmga.org/

The views and opinions expressed in this article are those of the author(s) and do not reflect those of Goldmoney, unless expressly stated. The article is for general information purposes only and does not constitute either Goldmoney or the author(s) providing you with legal, financial, tax, investment, or accounting advice. You should not act or rely on any information contained in the article without first seeking independent professional advice. Care has been taken to ensure that the information in the article is reliable; however, Goldmoney does not represent that it is accurate, complete, up-to-date and/or to be taken as an indication of future results and it should not be relied upon as such. Goldmoney will not be held responsible for any claim, loss, damage, or inconvenience caused as a result of any information or opinion contained in this article and any action taken as a result of the opinions and information contained in this article is at your own risk.