Central banks and gold

Mar 2, 2017·Alasdair MacleodThe very near future is likely to see a sea-change in central bankers’ attitude to the gold allocation in their reserves. The failure of G20 monetary policy since the financial crisis is causing a general rethink, which may eventually lead to a new policy direction.

For now, that is undecided, beyond a growing acceptance that today’s monetary policy does not work and the assumptions of recent decades, that gold as money should be phased out, might have been a mistake.

The idea, that Western central banks could banish gold from the monetary scene over time, has been disrupted by the persistence of Asian demand, fuelled by the remarkable economic progress of ex-communist states embracing capitalist methods. Western financial markets have hardly begun to grasp the wider implications of the shift in economic power from the heavily-indebted welfare economies, to China, Russia and other members of the Shanghai Cooperation Organisation, and their consequences for gold.

The welfare-driven states rely on money and credit expansion to conceal the true costs of their escalating government spending. They have been motivated to deny gold’s fundamental role as sound money, because it is superior to their unsound money. The increasing prosperity of Asians of all races, who still value gold for its ability to retain its purchasing power, ultimately undermines Western monetary policy, as well as the propaganda that goes with it.

The shift of physical demand from West to East has been widely chronicled, ever since the Shanghai Gold Exchange became a conduit for escalating physical demand. Inevitably, the West’s desire to demonise gold has accelerated the process, and we are now at the point where control of the gold price could suddenly shift from Western capital markets, trading in futures, deferred settlements and unallocated accounts, to the markets supplying bullion in Asia.

This article discusses the Eurasian geopolitical issues that are becoming increasingly important for the near-term future of the gold price, and why many central banks are likely to increase their gold reserves at a faster pace than in the recent past. It is a story which is partly political, but also now includes the consequences of the future failure of the Eurozone and its currency. The systemic failure of the Eurozone, raising fundamental questions for the euro’s future, and the risks attendant to other fiat currencies, can now said to be in plain sight.

Russia

We shall start with Russia. Something very interesting occurred last week: according to Izvestia, the Russian newspaper, Russia will pay off the only remaining debt of the old USSR. Terms have been agreed with Bosnia and Herzegovina for the payment of $125 million in final settlement, and this appears to be the last of the old debts, Russia having paid off the others and written off money owed to her by Cuba and several others indebted countries.

This raises the question as to why Putin, demon to the West, instead of reneging on these old debts, which surely an evil man would do, appears to be removing all international claims on the Russian government. Meanwhile, foreign currency debt owed by the Russian Government was about $40bn on 1st April 2016, and assuming it is unchanged, the rise in the rouble since then will have reduced it to only $30-34bn equivalent. Much of this debt is likely to be in currencies other than the dollar. It compares with a current annual trade surplus of $12bn, and oil exports that alone are worth about $100bn at today’s prices.

Russia’s national accounts are in reasonable shape as well, with the budget deficit for this year under 2% of GDP, assuming oil holds the $50 price per barrel level. Price inflation is forecast to fall to about 4% after hitting 12.9% at end-2015. In short, Russia has one of the healthiest set of government finances in the G20. The central bank, by pursuing sound money policies, has played an important role in stabilising the economy, despite trade and financial sanctions from the West, and the West’s attempts to destabilise it.

There is overwhelming evidence Russia was targeted by the American defence and intelligence establishment with a view to bankrupt it. American presence was noted in the Euromaidan clashes in 2014, and according to Seumas Milne of the Guardian, the US selected the administration that followed the ousting of President Yanukovych. Assistant Secretary Victoria Nuland in March 2016 confirmed in some detail the help given to Ukraine following Euromaidan, including over $760 million in assistance and two $1bn loans. US advisors served in Ukrainian ministries, as well as being embedded in the National Bank and related institutionsi.

These advisors were in place when Ukraine’s gold went missing, fuelling suspicions it was sequestered by the US. The destabilisation of Syria also had much to do with her relationship with Russia, both civil wars on foreign soil instigated by America and NATO.

There appear to be powerful elements in the US intelligence agencies still bent on driving Russia into bankruptcy, an objective that has failed miserably. It is the logical explanation behind the battle being fought between elements in the intelligence establishment and President Trump over future relations with Russia. Russia has won this one, and can now afford to await developments in the American government. So, why is the Russian Government paying off all those old USSR obligations?

Surprisingly, Russia has a history of honouring past obligations. But by doing so, Russia has cleared the decks to neutralise the impact of further financial sanctions. Alternatively, she sees global financial and systemic risk escalating, and wishes to insulate herself from it. For the first case, she has eliminated dependency on dollars as much as possible, which is the primary control mechanism deployed by America over regimes she does not like. For the second, there is indeed much to worry about close to her doorstep. It has become increasingly obvious that the EU and the Eurozone, Russia’s Western neighbour, have been heading for political disintegration and an economic, systemic and currency crisis, which has become unavoidable. When the worst happens, Russia’s banking system will survive, while the West’s will not.

Russia’s one remaining weakness, in Western minds at least, is foreign obligations in the private sector, and at current exchange rates these are estimated to be about $400bn. This is certainly a significant sum for an economy with a GDP of $1,300bn equivalent. But an omnibus figure of this sort tells us nothing about where and why these obligations exist, and of how much is in euros and dollars as opposed to the currencies of Russia’s neighbours.

As a sound money advocate, in relative terms at least, Russia’s central bank is likely to take the broad view that the private sector is not the state’s business. Instead of hoarding dollars against private sector obligations, she is getting on with accumulating gold in her reserves, and one can see why. The problem with owning dollars, and therefore US Treasuries and T-bills, is Russia becomes a creditor of a strategic opponent, who can potentially render these holdings worthless. The additional problem with owning euros and euro-denominated sovereign debt is Russia can be reasonably certain the euro will become valueless, as the Eurozone disintegrates. Russia is therefore detaching herself from both the dollar and the euro. That will leave Russia ending up with a reserve portfolio of mainly Asian currencies, particularly the yuan, and gold.

Gold has the further benefit to Russia of being the West’s Achilles heel. Merely by accelerating the rate at which she accumulates gold, Russia can destabilise the dollar. However, she is unlikely to take this course of action without provocation, and without acting in concert with China, whose economic future she increasingly shares.

China

Both Russia and China, by their actions, show they understand the strategic power of controlling physical gold, with China also having encouraged its citizens to buy it. And given China’s mercantilist plans, which over time should generate substantial wealth for her citizens, public demand for gold will continue to grow. Her problem is she still owns in her reserves about $1 trillion of dollars and US Government obligations. However, she is reducing it by stockpiling the commodities necessary for her expansionary 5-year plan.

It will take time for China to extricate herself from such a large quantity of dollars and dollar-denominated debt. But there will be a cross-over point, where the losses on these dollar reserves from a rising yuan/dollar exchange rate are less than the fall in the yuan cost of imported industrial materials. At that point, China’s interests will shift in favour of a gradual currency appreciation of the yuan, allowing the yuan to become the fiat currency of choice throughout the Asian continent.

Whether and when China follows through with such a policy, only time will tell. But what’s happening with China’s dollar reserves is clear to most Asian central banks, who at least liaise with each other in forums such as the Shanghai Cooperation Council, and the Eurasian Economic Union. They know it is only a matter of time before their own dollar reserves will lose value and relevance, because of China’s ambitious policy to minimise use of the dollar in both her trade settlements and foreign reserves.

It also places Japan in an awkward position. Notionally an ally of the US and at odds with China politically, her business interests lie very much towards China and South-East Asia. She should therefore on trade grounds reduce her dollar exposure, and she appears to be opting to smooth the path by promising to invest much of the proceeds in the US. In other words, she will swap dollars and dollar bonds for real assets, in the knowledge that her more important trade partners are also sellers of dollar paper.

Therefore, it looks like all Asian central banks are potential sellers of US debt. Central banks for the smaller South-East Asian nations must surely be tempted to jump the gun while they can, undermining confidence in the dollar for the whole region. For example, Thailand has $66bn of US Treasuries, and shifting just 10% into gold at current prices requires the purchase of 164 tonnes, difficult to achieve when other central banks are buying in the market.

The choice for central banks throughout Asia, whatever their strategic allegiances, is to replace dollar exposure with Japanese yen, Chinese yuan, or gold. We can eliminate the euro as a major currency, because of mounting doubts over its future. More on this follows below.

Petrodollars – a threatened species

China’s dominance in world trade and its voracious appetite for energy has changed forever the focus of the Middle East from the American dollar towards Asian markets and the Chinese yuan. However, it will take time for these oil exporters to have confidence in the yuan as an acceptable trading medium. In this respect, Iran is probably more advanced than Saudi Arabia, because the Saudis have hidden behind a long-standing and close relationship with America, negotiated in the early 1970s.

After Nixon ended the Bretton Woods agreement in 1971, the oil price rose sharply, spurred on by members of OPEC. Recognising the inevitable, President Nixon and Henry Kissinger laid the foundations for the petro-dollar, whereby Saudi Arabia’s surplus oil revenues would be used to purchase US Treasuries, and the Saudi oil fields would remain in the US sphere of influence. This gave an opening in the region for US banks, who also recycled dollars to finance the deficits of Latin-American countries. Thus, the petro-dollar was bornii.

Today, little if any oil from the Middle East is exported to America, so the agreement that led to the petro-dollar has little commercial basis today, other than the dollar is the world’s reserve currency, and a level of international reserves needs to be maintained. As part of the original deal, Saudi Arabia was protected by the US as a close ally, and her internal affairs would never be challenged, in return for which she would price her oil in dollars. Consequently, a strict and extreme form of Sunni Wahhabism has been allowed to persist, insulated from all social progress. Naturally, there would be increasing strains with a world that was moving on, and there is compelling evidence that Saudi interests have in that backdraft financed extreme Islamic terrorism, from Al-Qaeda to the Islamic State, with the support, tacit or otherwise, of the US.

However, since the twin-towers atrocity in New York in 2001, American protection of the Wahhabi state has come under increasing strain, particularly following President Obama’s unsuccessful ventures in the wake of the Arab Spring. By the time President Trump was elected, the petro-dollar agreement was effectively dead and buried. Furthermore, the oil price collapse in 2014-15 exposed the Saudi Government to a financial crisis, requiring it to dispose of US Government bonds. So here again, we see sellers of dollars, in this case forced by financial circumstances. Furthermore, Saudi Arabian commercial interests, along with those of the Gulf States and Iran, are now realigned with the rest of Asia, which is the market for the bulk of its oil.

Goodbye to the Eurozone and the euro

Finally, we turn to Europe. Long before last year’s Brexit vote, it was clear that the European political model, conceived in the wake of the Second World War, was outdated and unable to survive in the light of a changed world. Financial and trade power has shifted from the model of established trading blocks, such as the EU, in favour of emerging nations. Conceived along with NATO by America in the communist era, when the Soviets had to be contained, the EU is no longer relevant. Brexit merely exposed this fact.

The EU, being conceived out of and driven by political objectives, always ignored financial and economic reality. When it was decided to introduce the euro, countries like Italy, France, Spain, Greece and Portugal found their cost of borrowing in euros became a fraction of the previous cost of borrowing in lira, francs, pesetas, drachmas and escudos respectively. The result was an explosion of borrowing and state profligacy. Yet the inevitable credit crisis that follows a credit binge has been deferred and deferred. Eventually, the crisis will happen. It will be far larger through being put off, and everyone knows, or at least suspects it. However, the lack of economic progress in over-indebted EU economies is telling, and public discontent is mounting. And any EU national can now see that Brexit has created an attractive precedent, and that there is a better future in prospect outside this increasingly irrelevant union with its flawed currency.

For this reason, Brexit is ringing alarm bells in the establishment everywhere in Europe. In upcoming elections this year, the Netherlands, France and Italy, all being major components of the Eurozone, risk electing rebel administrations with policies aimed at escaping the EU’s straitjacket. And if the rebels are denied office this time, they will gain more support as a result.

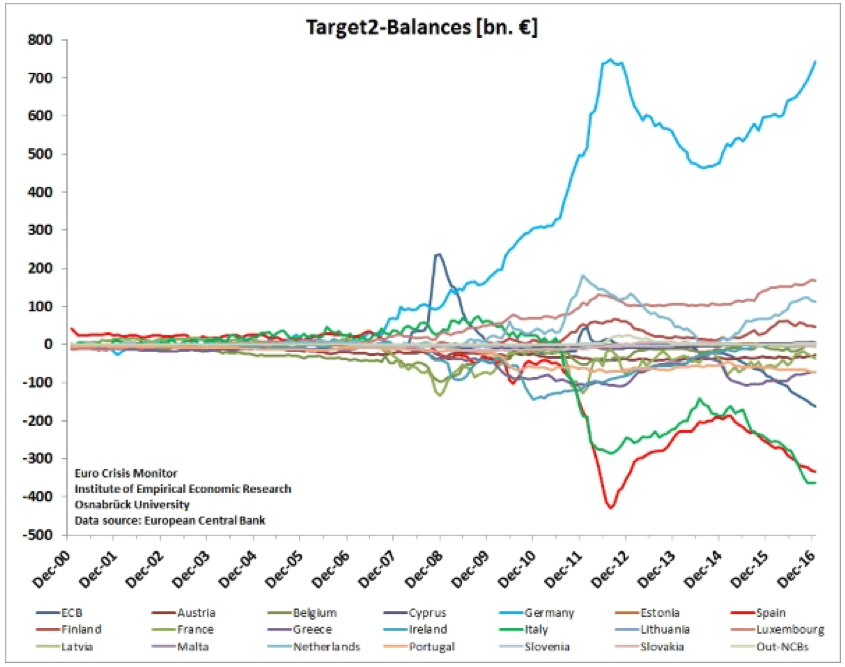

Already, we see capital flight ahead of this year’s political risks building to record levels, as Italians, the Spanish and the French, move money into German, Luxembourgeoise and Dutch banks. This capital flight is plainly reflected in increasing TARGET2 imbalances, illustrated below.

At the end of January, the Bundesbank reported its balance was at a new record high of €795.6bn, by far the largest component out of a total of over €1 trillion in imbalances, and an increase on last December. Nearly all of it is capital flight, as can be deduced from the low level of imbalances before the financial crisis of 2008, when systemic risk was not an issue.

How any resident of the Eurozone can think that there is safety in German banks is beyond logic, but there it is. The previous peak in late-2011 reflected the growing realisation across the Eurozone that money in Spanish and Italian banks was at risk, and German banks were regarded as safe. Capital flight creates strains, and eventually these surfaced in Cyprus over the following eighteen months, before her banks succumbed in March 2013.

The Cyprus crisis was handled with malice aforethought by the EU, which was determined to make an example of Cyprus and her tax-haven Russian clients, and to punish Russia for lending Cyprus an emergency loan of €2.5bn a year before, following the EU’s own refusal to help Cyprus. In the event, many Russians got their money out by various means, while the local population bore the brunt of the crisis.

What was less publicised was the surge in European demand for physical gold, leading to persistent reports that two major Dutch banks had halted transfers to customers from their unallocated accounts. Physical ETF holdings were at record levels.

The tightness of the physical market led to a coordinated bear-raid on gold, driving the price down sharply in April 2013 by targeting weak hands in physical ETFs. The operation was successful, defusing Western demand, but it allowed Chinese and Indian buyers to benefit. The net result is physical liquidity in Western markets declined significantly, and the market’s ability to absorb a surge in European demand today is restricted by the reduction in physical gold available in Western vaults.

Cyprus was tiny. Greece, which followed, was still small. Now we are faced with Italy. And before we get there, we have the Dutch debating in Parliament whether they should leave the euro. A series of elections in Italy, the Netherlands and France may or may not lead to the appointment of anti-establishment administrations, but it will almost certainly undermine the status quo. And as confidence in the political situation deteriorates, a process already begun and confirmed by TARGET2 imbalances, a sense of crisis is bound to escalate. Crucially, America, which created the forerunner of the EU in the late-1940s, for the first time has a president and administration that openly criticises it by backing Brexit.

Demand for physical gold, to escape the alternative of counterparty risk on deposits with Eurozone banks, is therefore bound to grow. The World Gold Council has reported a significant increase in demand from Germany last year. One suspects that the Eurozone area will be the first to see widespread gold buying by high net worth individuals, trying to protect themselves from a systemic event that has become all but certain, and will even threaten the entire banking system.

There is however one further issue, and that is what will happen to the Eurozone’s national central banks gold holdings as the Eurozone disintegrates. It could be demanded as part-collateral against bail-out loans from the IMF, and doubtless bullion banks will come up with propositions involving the transfer of national gold to their control. Alternatively, there is a case to be made for maintaining gold reserves to bolster confidence in the currencies that might be planned to replace the euro. This is likely to be a reason the Bundesbank recalled 411 tonnes of its gold held in New York and Paris, which would be useful to window-dress a new deutsche mark.

That is a worry for later. For the moment, we should just think for a moment about the effect on the whole Eurozone banking system, if perceptions spread that TARGET2 imbalances cannot be settled as the Eurozone disintegrates. We can be sure that central banks and sovereign wealth funds are monitoring this silent, deadly run on the Eurozone’s banking system, with increasing alarm. Before Brexit, they must of have hoped that the political will would always exist to defer and defuse a banking crisis. Not only is that no longer so, but it is increasingly difficult to make a case for the Eurozone’s survival. The problem is already becoming obvious to central banks and sovereign wealth funds, deciding how to allocate reserve assets. No government institution dares debate the collapse of the EU in public, for fear of precipitating the inevitable crisis.

Conclusion

Most exporting nations accumulating foreign currency reserves are turning into sellers of dollars. This is either for strategic reasons, such as in the case of Russia and China, or because their commercial interests are becoming increasingly aligned with Sino-Russian trade policies. China, Russia, Japan and the Middle East are therefore all future sellers of the dollar, and of the underlying US Treasuries and T-bills in their possession. All other central banks will also be aware of these developments by now, and should be re-examining their exposures accordingly.

The coming months will almost certainly see a further deterioration of the Eurozone’s survival prospects, and an objective analysis must embrace the consequences of its demise and that of the whole euro financial system. The only way capital flight within the system can be reconciled is by a systemic collapse. That puts two major reserve currencies on the sell list of most central banks: the dollar and the euro.

Together, they are the world’s reserve currency and the currency for the world’s next largest economic area. They account for 40% of the world’s GDP, the part that represents the world of yesterday. Therefore, there is a sea-change underway in nearly all central banks attitude to gold, if only because other than the yen, yuan, sterling and the Swiss franc, what else is there?

i Testimony to Senate Foreign Relations Committee Hearing, March 2016

ii See https://www.bloomberg.com/news/features/2016-05-30/the-untold-story-behind-saudi-arabia-s-41-year-u-s-debt-secret for a description of the creation of the petro-dollar.

The views and opinions expressed in this article are those of the author(s) and do not reflect those of Goldmoney, unless expressly stated. The article is for general information purposes only and does not constitute either Goldmoney or the author(s) providing you with legal, financial, tax, investment, or accounting advice. You should not act or rely on any information contained in the article without first seeking independent professional advice. Care has been taken to ensure that the information in the article is reliable; however, Goldmoney does not represent that it is accurate, complete, up-to-date and/or to be taken as an indication of future results and it should not be relied upon as such. Goldmoney will not be held responsible for any claim, loss, damage, or inconvenience caused as a result of any information or opinion contained in this article and any action taken as a result of the opinions and information contained in this article is at your own risk.